Should you refinance your home or take on a reverse mortgage?

Heading into retirement? Here’s how you can secure both a roof over your head and cash in your pocket.

When people think about paying off their mortgage, they often feel a sense of dread. The idea of being stuck with a huge debt for years is daunting, so we tend to want to pay off our mortgage as soon as possible. We might even dip into our EPF to do it, believing that getting rid of this

financial burdenis the key to financial freedom.

But what happens when you finally retire? Yes, your house is paid off, but what if your cash reserves aren’t enough to sustain your lifestyle for the next 30-odd years? Many retirees face this problem of owning a fully paid-off home but not having enough liquid cash to live comfortably

So, where can you get the cash you need? Do you sell your house? But then, where would you live? Should you consider refinancing? But how can you get a loan without steady income during retirement?

These are common concerns among retirees. While having a paid-off home saves you on housing costs, other expenses – like healthcare, medical bills, and daily living costs – still need to be covered.

What’s worse is that you might outlive your savings: what happens to all the money you’ve saved if you don’t spend it before you die?

One viable option might be to refinance your house, which would give you access to cash you could use to enjoy your retirement. By refinancing, you can unlock the value of your home and access cash, giving you more freedom and flexibility.

Instead of sacrificing your quality of life to own a paid-off home, you could enjoy a more comfortable retirement.

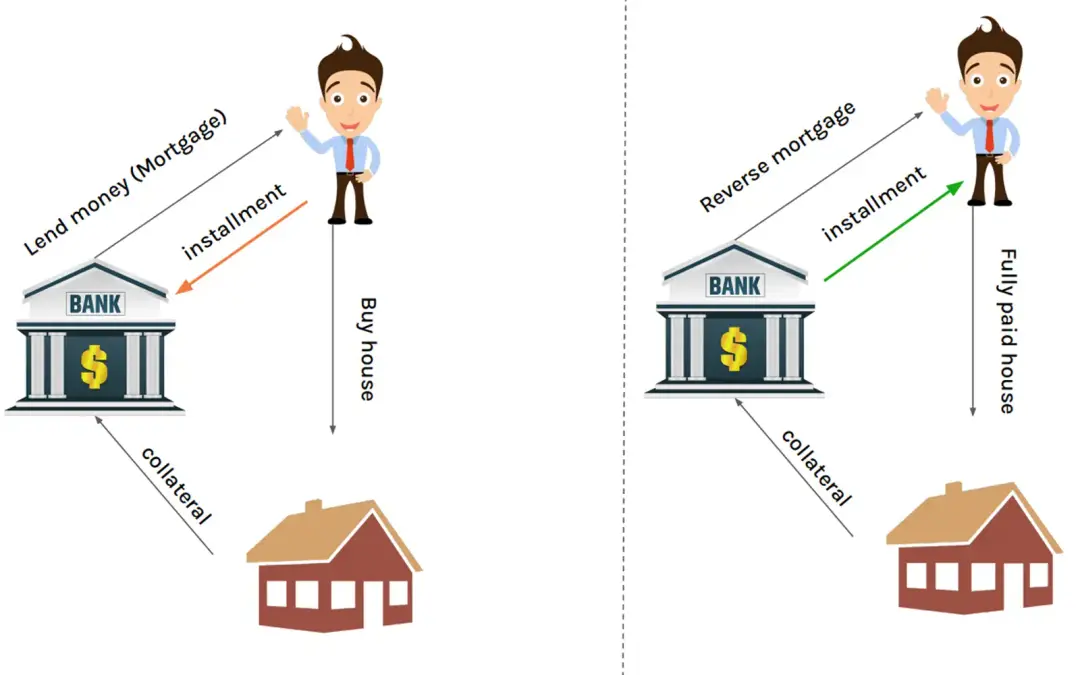

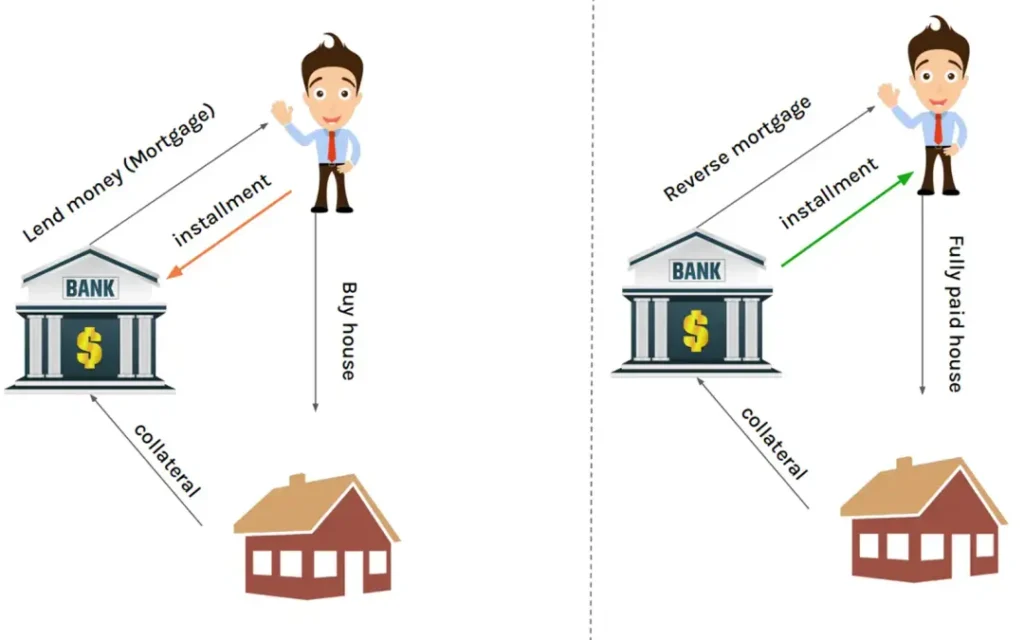

The reverse mortgage

If refinancing doesn’t sound appealing, here’s another option: a reverse mortgage. This financial product allows retirees to unlock the value of their home without selling it or making monthly loan payments. It is an attractive alternative for those who wish to live in their home while accessing additional cash.

A reverse mortgage is different from a traditional one. You don’t make payments to the lender; instead, the lender makes payments to you, based on a percentage of your home’s value. You can receive this money as a lump sum, monthly payments, or a line of credit.

The loan is typically repaid when you sell the home, move out, or pass away. Notably, with a reverse mortgage, you retain ownership of your home and can continue living in it. The loan is secured by your home, and the interest is added to the loan balance each month.

Over time, as you receive payments and interest accrues, your equity in the home decreases.

While reverse mortgages can be a good way to free up cash during retirement, the financing cost can be significantly higher than a regular mortgage – in some cases up to 50% more expensive than a typical mortgage.

This higher cost means that, while a reverse mortgage can provide immediate financial relief, it’s essential to weigh the long-term impact on your home equity. As the interest compounds, the amount you owe can grow quickly, potentially leaving less inheritance for your heirs.

How to use your cash after refinancing

Once you refinance and have cash in hand, what should you do with it? Here are a few suggestions:

Put it into higher-return investments

Consider putting your money into investments with higher returns, which can help you grow your wealth while keeping cash on hand for your needs.

If you’re working with a substantial amount, consider consulting multiple fund managers and directly engaging one to manage your portfolio.

Look for managers with a strong track record who focus on value investing and understand how to manage risk. A good manager should be able to deliver returns of more than 10% a year after fees over the long term.

Put it back into EPF

If you’re not comfortable with high-risk investments, putting the money back into your EPF is a solid option. With EPF offering a dividend rate of over 5% and mortgage rates under 5%, you can still earn a net return.

Invest in stable financial products

You could also look into other stable financial products like bonds or high-yield REITs. While these might not offer the highest returns, they’re stable and can provide a reliable cash flow for your retirement.

The key is to make your money work for you, instead of locking it all up in your house. This way, you can enjoy your retirement while ensuring financial stability and freedom.

Leave a Reply